The Most Popular Crypto Cards in January 2026

On-chain settlement data offers rare insight into how crypto cards are actually used. January 2026 volumes reveal which payment models are gaining real traction.

The data referenced in this article is sourced from Dune Analytics and was compiled by researcher @obchakevich. It aggregates on-chain settlement activity across multiple blockchains and card programs, providing a usage-based view of crypto card adoption rather than marketing claims or account counts.

Transaction volume is not a measure of product quality or user satisfaction. However, in the context of crypto payments, it remains one of the strongest indicators of sustained real-world usage, reflecting successful conversion, settlement reliability, and merchant acceptance.

Why on-chain volume matters for crypto cards

Crypto cards operate across both on-chain and off-chain payment rails. A single card payment may involve smart contracts, liquidity pools, custodial balances, card issuers, and traditional acquiring banks before final settlement. Each provider chooses a different architecture.

Because of this complexity, many announced crypto card programs never reach meaningful usage. On-chain settlement volume helps filter out inactive or lightly used products by focusing on value that actually moves through crypto-native infrastructure.

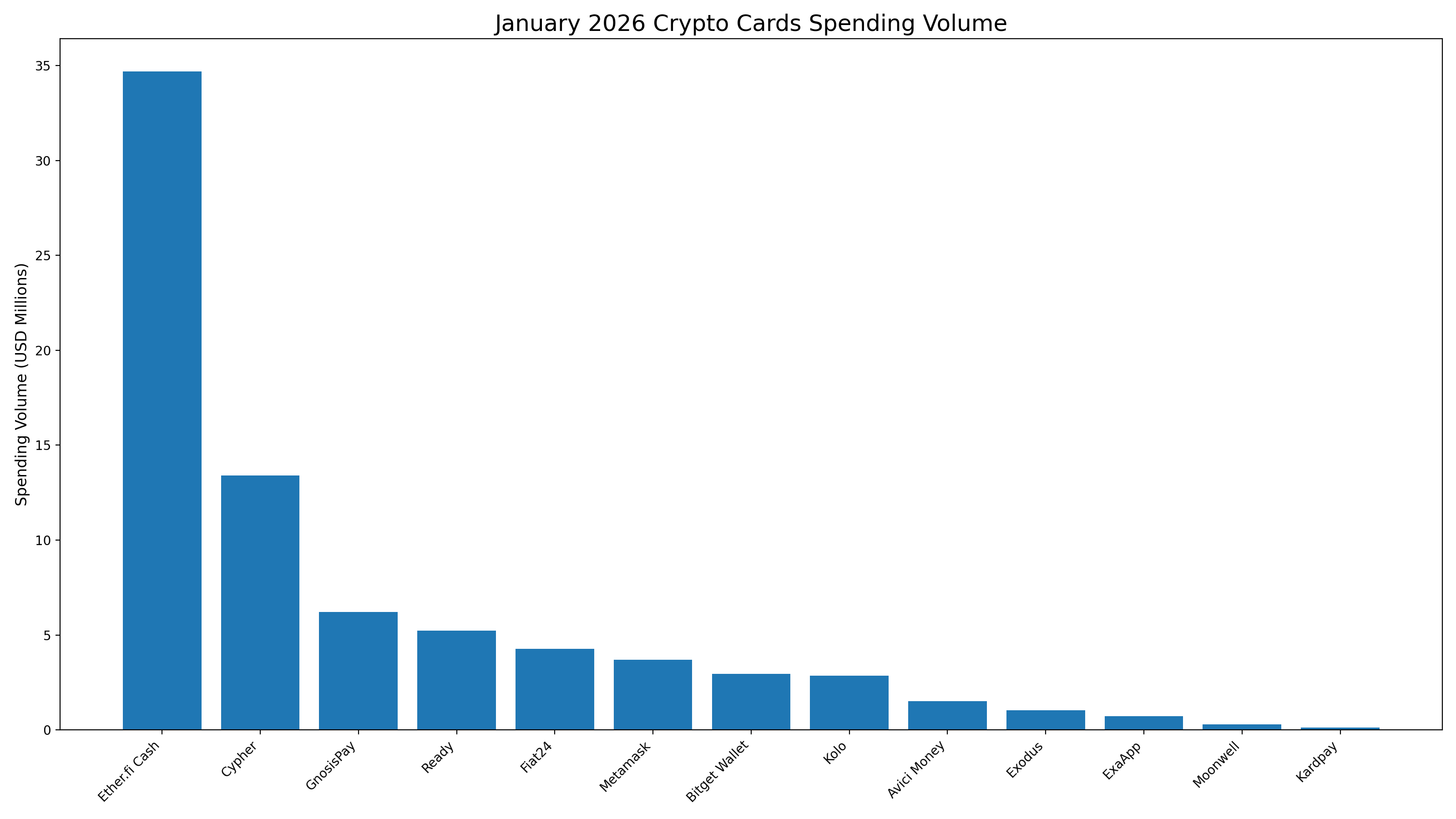

January 2026 volume overview

January 2026 data shows a clear concentration of volume among a small group of crypto card programs. These leaders are not unified by a single custody or funding model, but they do share relatively mature settlement pipelines and consistent transaction flow.

The distribution also highlights how different card architectures scale at different rates. Wallet-native debit cards, protocol-linked spending accounts, and collateral-backed credit cards each show distinct volume profiles.

Ether.fi Cash and protocol-linked spending

Ether.fi Cash recorded the highest on-chain card settlement volume in January 2026. Its activity reflects growing demand for spending mechanisms tied directly to protocol-level balances rather than exchange accounts or preloaded custodial wallets.

Instead of treating card spending as a separate financial silo, Ether.fi Cash integrates spending access into a broader staking and yield environment. This reduces friction for users who want liquidity without fully exiting on-chain positions.

A structural overview of this approach is available here: Ether.fi Cash card.

Source: Dune @obchakevich

Gnosis Pay and DAO-native payment flows

Gnosis Pay ranked among the top programs by January volume. Its usage is closely tied to DAO operators, multisig treasuries, and teams that already manage funds on-chain.

Rather than targeting retail onboarding, Gnosis Pay extends treasury infrastructure into everyday payments. This model aligns card usage with operational spending, such as subscriptions, travel, and vendor payments.

More information on its settlement and custody structure can be found here: Gnosis Pay card.

MetaMask Card and self-custodial debit spending

MetaMask Card continued to generate meaningful transaction volume in January. Its growth reflects demand for self-custodial spending, where assets remain under user control until the moment of payment.

This approach minimizes the need for prefunded custodial balances, but it also increases dependency on wallet UX, gas efficiency, and real-time conversion reliability. As volume grows, these operational details become increasingly important.

A breakdown of supported assets and payment mechanics is available here: MetaMask Card.

Bitget Wallet and integrated wallet cards

Bitget Wallet Card recorded mid-tier volume, reflecting steady usage among users who prefer an all-in-one wallet environment. Funding, asset management, and spending occur within the same interface.

This design reduces friction between holding crypto and spending it, but it also relies more heavily on custodial or semi-custodial infrastructure depending on region and issuing partner. These trade-offs vary by jurisdiction.

Additional structural details are available here: Bitget Wallet Card.

Fiat24 as underlying banking infrastructure

Fiat24 itself appears in January data primarily through cards that operate on top of its banking and settlement layer. Rather than functioning as a consumer wallet, Fiat24 provides regulated fiat rails connected to on-chain identity and balances.

This model allows partner wallets to offer card access while outsourcing traditional banking integration. Spending volume attributed to Fiat24-backed cards reflects both the strength of this abstraction and its growing partner ecosystem.

SafePal and Fiat24-backed card programs

SafePal’s card usage illustrates how wallet providers can leverage Fiat24 infrastructure without building their own banking stack. In this setup, the wallet handles crypto custody while fiat settlement and card issuance are abstracted away.

This separation simplifies compliance and banking access, but it also introduces dependencies on third-party settlement timelines and account controls.

A structural overview of this arrangement is available here: SafePal card.

Avici and collateral-backed card spending

Avici Money recorded lower absolute volume than debit-focused cards, but its usage reflects a different spending paradigm. Instead of selling assets, users borrow against stablecoin collateral to fund card payments.

This approach treats the card as an extension of on-chain credit. It prioritizes capital efficiency and asset control, but it introduces liquidation risk and requires more active balance management.

Details on Avici’s custody and settlement mechanics are available here: Avici Money card.

What the volume data does not show

On-chain volume does not capture failed transactions, declined merchants, FX spreads, or user churn. A card program may process significant volume while still delivering inconsistent user experience.

Volume also aggregates very different usage patterns. Operational treasury spending, consumer subscriptions, and one-off purchases all appear identical in raw settlement data.

Structural trends emerging in 2026

January 2026 data highlights a fragmented but maturing crypto card ecosystem. There is no single dominant architecture. Instead, different models scale within their respective niches.

Protocol-linked spending, self-custodial debit cards, wallet-integrated cards, and collateral-backed credit products all coexist. Future growth is likely to depend more on infrastructure reliability and regulatory clarity than on rewards or branding.